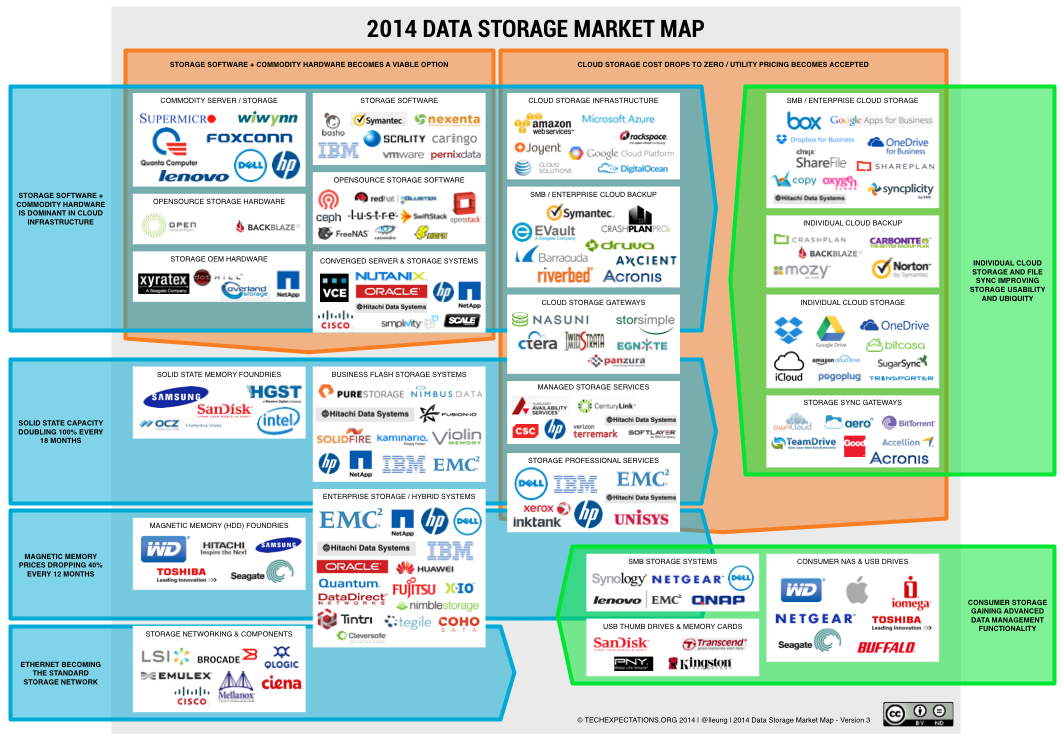

Data storage is a massive market ($22.5 billion for the 2013 high end storage market alone), and has reached a critical point in its evolution, highlighted by dramatic changes in base technologies, interfaces, and service models. EMC’s recent acquisition of DSSD was another thought-provoking data point.

- Hardware commoditization and component improvements have been a big part of the story. Magnetic storage has continued its relentless increase in density (Kryder’s Law), albeit with an extended pause in price declines due to a supply constraint from the Thai floods. Solid state storage is making significant inroads into enterprise and cloud data centers, pushing massive valuations for both enterprise flash vendors ($3 billion for Pure Storage), and flash-based cloud vendors ($153 million for Digital Ocean). Acceptance of x86 architectures for high scale storage systems, paired with open source hardware designs and scale-out software, has reached a pinnacle. Quanta Computer’s emergence as a direct system supplier and Red Hat’s acquisition of Ceph professional services firm Inktank are relevant data points there.

- Interfaces are a second area of dramatic change. Storage vendors took time to recognize it, but every automatic photo upload and default document save to the cloud means one more file diverted from traditional enterprise storage. If 2013 was the year when device sync solutions for individuals and groups ran rampant, 2014 is when business adoption reaches real scale. Home storage products, on a lesser scale, have also dramatically improved their interfaces, subsuming capabilities like video and music streaming, and cloud backup.

- Finally, cloud storage services have further upped the ante for individuals and groups, mostly with dramatic price drops. On March 17, Google Drive made one terabyte of storage available for only $10 a month, outpacing every competitor for individual cloud storage. They followed a week later by dropping Google Cloud Storage pricing by 68% to $0.026/GB/mo, making a platform for other services and applications considerably less expensive as well. AWS and Microsoft Azure quickly followed suit.

The 2014 Data storage market map is an attempt to capture these dynamics and the field of vendors in one picture:

2014 Data Storage Market Map by Leo Leung is licensed under a Creative Commons Attribution-NoDerivatives 4.0 International License.

May 13, 2014 at 8:30 am

Good luck, Leo. I’m very proud of you!

May 14, 2014 at 6:57 pm

Leo,

Congrats on the new blog and this insightful post.

I’d like to offer a few areas where I think you missed Hitachi, but instead of trying to get it all out in this comment, I went ahead and responded here in long-form…

https://community.hds.com/people/rmadaio/blog/2014/05/14/raising-hitachis-tech-expectations

Will be interested in thoughts!

Bob (a Hitachi guy) 🙂

June 10, 2014 at 6:53 am

Reblogged this on and commented:

Data storage market overview: State of the market in 2014

Pingback: 2015 Data storage market review: continued disruption by flash, SDS, and cloud | Tech Expectations